Intel’s Big Arizona Gamble: First U.S.-Made 2nm Chip Could Put America Back on Top

Intel’s Big Arizona Gamble: First U.S.-Made 2nm Chip Could Put America Back on Top

The chip giant unveils Panther Lake, built on its new 18A process, as the fight for semiconductor dominance heats up.

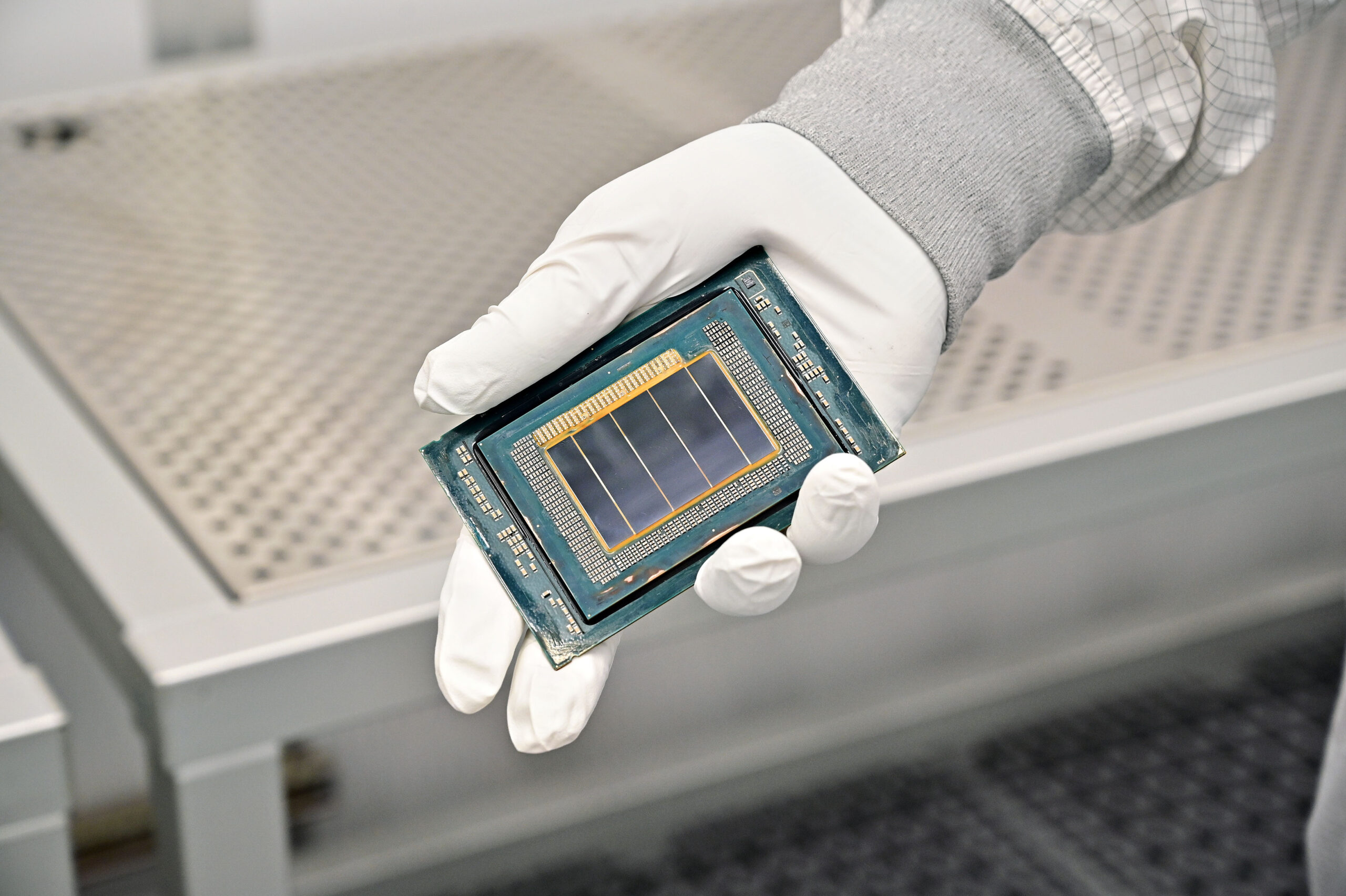

CHANDLER, Arizona — Intel just rolled the dice in the semiconductor war, and it’s a bold one. On October 9, the company pulled back the curtain on Panther Lake, a laptop processor designed and manufactured entirely on U.S. soil. This isn’t just another product launch. For Intel, it’s a statement: after years of playing catch-up, the company believes it’s ready to reclaim the technological crown it once wore so comfortably.

The Panther Lake Core Ultra 3, set to ship in consumer devices by January 2026, will be the first chip built on Intel’s 18A process node. The new silicon comes from Fab 52, Intel’s massive Chandler facility that’s part of a $100 billion expansion project across the United States. With it, Intel promises the most advanced chips ever produced domestically—featuring breakthroughs like backside power delivery and next-gen transistors. Analysts say these innovations could give the company a rare, if temporary, lead over Taiwan Semiconductor Manufacturing Co. .

“This is where PowerPoint slides turn into real silicon,” one semiconductor analyst quipped. “If Intel nails yields and power efficiency, it could actually hold process leadership again, at least for a little while.”

Power From the Backside: Intel’s Secret Weapon

So what makes this chip special? At its core is a technology Intel calls PowerVia. Think of it as rerouting traffic. Traditional chips send both data and electricity across the same “road” on the wafer’s top side, creating congestion. Intel flipped the script—literally—by moving power delivery underneath the chip. That frees up space for signals and cuts voltage loss, which in theory boosts both efficiency and performance.

Timing may be Intel’s ace. TSMC’s rival N2 node is scheduled for mass production in late 2025 but won’t feature backside power delivery. That upgrade won’t appear until its A16 node in late 2026. If Intel keeps its promises, the company could enjoy a 12–18 month head start in performance per watt.

Alongside PowerVia, Intel is rolling out RibbonFET, its first new transistor design in more than a decade. This “gate-all-around” setup reduces current leakage and makes scaling easier, another way to squeeze more out of every square millimeter of silicon.

Whether these advances actually extend battery life—the metric laptop buyers notice most—remains to be seen. Early production chips often sacrifice clock speed for yield, and laptops have little tolerance for thermal trade-offs.

AI Arms Race: Intel Aims for 180 TOPS

Performance isn’t only about raw speed anymore. Panther Lake is designed to deliver up to 180 trillion operations per second across its CPU, GPU, and neural engines. Intel dubs this “platform TOPS,” pushing back against competitors who tout only NPU numbers. Why? Because in the real world, AI workloads often bounce to graphics processors instead of running on dedicated AI silicon.

But Intel won’t have an easy ride. AMD’s Ryzen AI 300, already on the market, offers around 50 TOPS while sipping power efficiently. Qualcomm’s Snapdragon X2 Elite, expected in early 2026, targets 80 NPU TOPS, leaning on ARM’s reputation for stellar battery life. Apple’s M4 may only hit 38 NPU TOPS, but thanks to Apple’s tight integration of hardware and software, it still sets the gold standard for sustained performance on battery.

“The TOPS number on its own is meaningless,” one analyst warned. “Memory bandwidth, thermal design, and software maturity decide whether 180 TOPS feels fast or just looks good on a slide.”

To maximize flexibility, Intel is betting on a modular, multi-chiplet design. The compute die, made on 18A, houses CPU cores, the NPU, and a media engine, while other tiles handle graphics and I/O. That approach helps yields and costs but could introduce latency compared to one-piece designs.

The $143 Million Unit Question

The stakes are enormous. Analysts expect around 143 million AI-capable PCs to ship in 2026, roughly half the total PC market. This shift toward AI-ready machines is fueled in part by enterprises upgrading before Windows 10 reaches end-of-life in October 2025. For Intel, even a small bump in market share here could translate into billions of dollars.

If Panther Lake shines in real-world use cases—say, video calls with instant background blur, faster content creation, or on-device AI summarization—it could ride the wave of corporate refresh cycles. On-device AI doesn’t just mean speed; it also reduces latency, improves privacy, and avoids recurring cloud costs. That’s particularly appealing to regulated industries and budget-conscious IT departments.

Arizona as Ground Zero

Intel’s new Fab 52 isn’t just another factory. It’s the only Western facility capable of producing leading-edge logic chips at scale, a fact that carries serious geopolitical weight. After pandemic-era shortages and growing tensions around Taiwan, Washington has made semiconductor sovereignty a national security priority.

The Chandler plant is slated to hit volume production in late 2025, with customer shipments by year’s end and broader availability in early 2026. Success would not only vindicate Intel’s enormous capital outlay but also attract outside customers to its foundry business—an area where it’s desperate to gain ground on TSMC and Samsung.

Failure, on the other hand, would rekindle doubts about whether Intel spread itself too thin by overhauling its technology, expanding capacity, and reinventing its business model all at once.

What to Watch in 2026

Investors shouldn’t just listen to Intel’s marketing. Several telltale signs will reveal whether Panther Lake lives up to the hype. Independent reviews that normalize performance against battery life will be crucial. Design wins across Dell, HP, and Lenovo will matter far more than one flashy showcase device. And, of course, yields and clock speeds will determine if Panther Lake becomes the industry standard or another short-lived experiment.

The wildcard remains ARM. Qualcomm is improving Windows compatibility and pushing its own efficiency edge. If ARM-based Windows laptops reach parity in performance while still offering longer battery life, Intel’s decades-long x86 dominance could erode just when it needs pricing power most.

Analysts caution investors to separate Intel’s manufacturing milestone from its market prospects. Fab 52 proves Intel can still build cutting-edge chips in the U.S., which alone could unlock new foundry revenue streams. But winning sustained PC market share will hinge on execution—battery life, software optimization, and yields—factors that won’t be clear until real devices ship at scale.

The Bottom Line

In the semiconductor industry, specs on paper often mean little compared to what ships in laptops and desktops worldwide. Intel’s Panther Lake on 18A is its most credible shot in years at reclaiming technological leadership. Whether that translates into a lasting competitive edge depends on three unforgiving metrics: battery life, customer adoption, and production yields.

If Intel can deliver on those, it won’t just be a comeback story—it’ll be a turning point for American chipmaking.

House Investment Thesis

| Category | Summary & Key Points |

|---|---|

| Overall Thesis | Panther Lake on 18A is a credible sign of Intel's turnaround. A successful high-volume launch in Jan '26 would be a manufacturing breakthrough with a transient node leadership, but product leadership is unproven. The outcome is a binary skew on execution. |

| What's New | • Node: 18A with RibbonFET + PowerVia (backside power) in volume, ahead of TSMC's A16 (H2'26). • Performance: ~180 Platform TOPS (CPU+GPU+NPU), up from ~120. • Manufacturing: High-Volume Manufacturing (HVM) at Fab 52 in Arizona, aligned with CHIPS Act and secure supply demands. |

| Market Context | • AI-PC TAM: ~31% share in 2025 (~78-103M units), growing to ~50%+ by 2026 (~140M units). • Catalyst: Windows 10 End-of-Life (Oct 2025) driving enterprise refresh cycle. • Gating Factor: Execution-to-experience (battery life, software stability) over raw TOPS. |

| Competitive Position (2025-26) | • AMD Ryzen AI 300: ~50 NPU TOPS, strong CPU perf/W, incumbent x86 threat. • Qualcomm Snapdragon X2: ~80 NPU TOPS, ARM perf/W threat; could make Windows-on-ARM "good enough". • Apple M4: Ecosystem benchmark for perf/W. • Process Edge: Intel has a credible near-term manufacturing lead with 18A volume. |

| Technology Appraisal | • PowerVia: Real advantage (frees routing, reduces IR drop, improves utilization); key is yield/variability. • Platform TOPS: Bet on CPU/GPU/NPU combo is sensible, but real-world wins depend on software routing & thermals. • Chiplets (Foveros): Provides SKU flexibility and yield harvesting, aiding gross margins. |

| Financial Implications | • Revenue/ASP: AI-PC mix should lift mobile CPU ASPs. • Gross Margin: Positives (pricing power, chiplet binning, secure supply premia) vs. Negatives (first-gen node yields, fab start-up costs). • Capex/Opex: High but necessary for 18A HVM and Intel Foundry Services (IFS) credibility. |

| Bull Case (Inflection) | 1. Competitive 18A yields by mid-'26. 2. Top-tier OEM breadth at launch. 3. Battery-normalized leadership vs. AMD & near-parity vs. ARM. 4. ISV proofs showing end-to-end latency wins. 5. IFS credibility boosted by server (Clearwater Forest) on 18A. |

| Bear Case (Risks) | • Yields/thermals disappoint → down-binned parts, lost OEM slots. • Windows-on-ARM crosses the chasm → structural x86 pressure. • Platform TOPS doesn't translate to user experience. • CHIPS Act optics/funding change. |

| Key KPIs to Track | • 18A yield/defect density & bin splits. • Independent, battery-normalized performance reviews vs. Ryzen AI 300 & Snapdragon X2. • Design-win breadth & enterprise shelf presence in Q1'26. • Fab 52 wafer outs & cost absorption. |

| Competitive Scorecard | • Process Tech (2025-mid-26): Advantage Intel (18A volume with backside power). • CPU Perf/W: Edge: Apple; watch Qualcomm in 1H'26. • NPU TOPS: Edge: Qualcomm (raw NPU); Intel bets on platform. • Ecosystem: Edge: x86 (Intel/AMD) in 2025; could narrow by 2026. |

| Final Verdict | • Ground-breaking? Manufacturing: Yes. Shipping client volume with backside power ahead of peers is an industry first. Product: Promising but unproven. • Leading? Process lead: Likely. Product lead: Not yet (awaits third-party data). |

NOT INVESTMENT ADVICE