US Loses Triple-A Credit Rating - The End of an Era and What It Means for Markets

US Loses Triple-A Credit Rating: The End of an Era and What It Means for Markets

In a historic blow to America's financial standing, Moody's Ratings downgraded the United States' sovereign credit rating from "Aaa" to "Aa1" on Friday, stripping the nation of its last remaining triple-A credit rating and marking the first time in history that the U.S. holds no top-tier ratings from any major agency. The one-notch reduction, though anticipated by some market watchers, represents a watershed moment for the world's largest economy and reserve currency issuer.

Summary of Sovereign Credit Ratings and Major Rating Agencies: This table outlines the key global agencies that assign sovereign credit ratings, their rating scales, and the general classification of credit tiers. These ratings assess a country's ability to repay debt.

| Agency | Rating Scale (Highest to Lowest) | Investment Grade Range | Speculative Grade Range | Notes |

|---|---|---|---|---|

| Moody’s | Aaa, Aa1, Aa2, ..., C | Aaa to Baa3 | Ba1 to C | Uses numbers within letter grades (e.g., Aa1) |

| Standard & Poor’s (S&P) | AAA, AA+, AA, ..., D | AAA to BBB– | BB+ to D | Uses plus/minus to refine letter grades |

| Fitch Ratings | AAA, AA+, AA, ..., D | AAA to BBB– | BB+ to D | Same scale as S&P |

"It's a formal recognition of America's deteriorating fiscal trajectory," said a veteran fixed-income strategist at a major Wall Street firm. "We've crossed a Rubicon that many thought impossible even a decade ago."

The Breaking Point: Fiscal Paralysis Amid Ballooning Debt

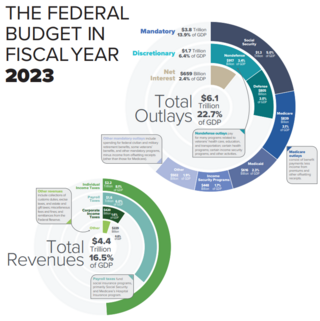

Moody's decision came as U.S. debt metrics reached levels "significantly higher than similarly rated sovereigns" with little political consensus on meaningful fiscal reform. The rating agency highlighted projections showing federal deficits widening from 6.4% of GDP in 2024 to nearly 9% by 2035, with the national debt burden expected to balloon to approximately 134% of GDP over the same period, up from 98% today.

Did you know that according to rating agencies, the US federal debt as a percentage of GDP is projected to reach alarming levels, rising from approximately 98-100% in 2024 to between 118% and 134% by 2035, marking the highest debt-to-GDP ratio in American history? This concerning fiscal trajectory, which recently prompted Moody's to downgrade the US government's credit rating, is driven by persistent large deficits expected to approach 9% of GDP by 2035, with interest costs alone projected to consume around 30% of federal revenue (up from 18% in 2024) and reach nearly $1.8 trillion annually by 2035-more than double current levels. Contributing factors include increasing mandatory spending, potential extensions of tax cuts, and rising interest payments on existing debt, collectively raising serious concerns about America's long-term fiscal sustainability.

The timing couldn't be more pointed. Just hours before the downgrade announcement, President Trump's ambitious tax reform proposal—which would extend his 2017 tax cuts and potentially add $4 trillion to the federal deficit over the next decade—failed a critical procedural hurdle in Congress. Hardline Republicans blocked the legislation, demanding deeper spending cuts as the federal debt has already swelled to approximately $36.2 trillion.

"When mandatory spending including interest payments consumes 78% of your budget by 2035, you've lost meaningful fiscal flexibility," noted an economist specializing in sovereign debt dynamics. "That's the trajectory Moody's sees, and it's what triggered this historic action."

Market Reaction: Subtle Tremors With Long-Term Implications

The immediate market response proved relatively contained but meaningful. Treasury yields climbed in late Friday trading, with the benchmark 10-year yield rising to 4.49%. An ETF tracking the S&P 500 declined 0.6% in after-hours trading, while gold pushed above $3,200 per ounce—reinforcing its safe-haven narrative.

Did you know that on May 16, 2025, Moody's downgraded the United States' credit rating from "Aaa" to "Aa1," marking the end of America's top-tier credit status across all major rating agencies, which caused an immediate market reaction as the 10-Year Treasury yield reversed its earlier decline and jumped to 4.499% following the announcement, reflecting investor concerns about the country's fiscal outlook including projections that federal debt could reach approximately 134% of GDP by 2035 and deficits could approach 9% of GDP, all while the Treasury market was already experiencing its longest slide of the year with three consecutive weeks of losses?

Five-year U.S. credit default swaps, which function as insurance against default, have widened to 56 basis points—their highest level since the debt ceiling standoff in 2023. While still far from crisis levels, this widening suggests institutional investors are increasingly hedging against tail risks in Treasury markets.

//DID_YOU_KNOW_INSERT:{"caption":"What are Credit Default Swaps (CDS)?", "search_queries":["credit default swaps explained for investors", "how do CDS work sovereign debt", "CDS as measure of country risk"]}

The muted immediate reaction masks deeper structural concerns. As one global macro hedge fund manager explained: "The first-ever loss of all three triple-A stamps is symbolically devastating but mechanically subtle. I expect only a 10- to 20-basis-point term-premium repricing in the near term, but this plants a durable seed of doubt about U.S. fiscal discipline that could blossom into meaningfully higher real rates over the coming decade."

Summary of Term Premium in Bonds: This table outlines the definition, significance, causes, and estimation methods of the term premium, which represents the extra yield investors demand for holding long-term bonds due to additional risks.

| Aspect | Details |

|---|---|

| Definition | Extra return on a long-term bond over expected short-term rates |

| Formula | Term Premium = Long-term yield − Expected average short-term rates |

| Purpose | Compensates for risks of holding longer-duration bonds |

| Key Risks Priced In | Interest rate risk, inflation uncertainty, market volatility, liquidity |

| When Positive | Investors require more return for riskier long-term exposure |

| When Negative | Strong demand for long-term bonds (e.g., during crises or QE) suppresses yield |

| Economic Impact | Influences yield curve shape and central bank policy interpretation |

| Estimation Models | ACM Model (NY Fed), Kim-Wright Model (Fed) |

The Triple-A Club: America's Departure Leaves a Vacuum

The U.S. now joins a growing cohort of former triple-A sovereigns that includes the United Kingdom, France, and Japan—all downgraded over the past two decades as debt levels climbed following various economic crises. This leaves only a handful of nations—including Australia, Germany, Singapore, Switzerland, and the Nordics—in the exclusive club of triple-A rated economies.

Moody's was the last holdout among major rating agencies. S&P Global Ratings first lowered the U.S. rating in 2011 during another debt ceiling showdown, while Fitch Ratings downgraded the country in August 2023. According to a Moody's spokesperson, this marks the first time the agency has ever downgraded U.S. sovereign debt in its history—a testament to the significance of the decision.

Table: US Sovereign Credit Rating Changes by Major Rating Agencies (2011-2025)

| Year | Rating Agency | Previous Rating | New Rating | Key Reasons for Change |

|---|---|---|---|---|

| 2011 | S&P Global | AAA | AA+ | Concerns about debt management plan; weakened political institutions; difficulties in bridging partisan fiscal policy gaps |

| 2023 (August) | Fitch Ratings | AAA | AA+ | "Steady deterioration in standards of governance over 20 years"; debt ceiling standoffs |

| 2023 (November) | Moody's | Aaa (Stable) | Aaa (Negative Outlook) | Warning signal preceding potential future downgrade |

| 2025 (May 16) | Moody's | Aaa | Aa1 | Increased government debt and interest payment ratios significantly higher than peer countries; projected federal deficits widening to 9% of GDP by 2035 |

This table summarizes the sovereign credit rating downgrades of the United States by the three major credit rating agencies (S&P, Fitch, and Moody's) between 2011 and 2025. As of May 17, 2025, for the first time in modern history, the US no longer holds a top-tier AAA/Aaa rating from any major rating agency, potentially affecting borrowing costs and the country's status as a premier destination for global capital.

Despite the downgrade, Moody's acknowledged America's enduring strengths, citing "the size, resilience, and dynamism of its economy, along with the ongoing status of the dollar as the global reserve currency." The agency revised its outlook from negative to stable, suggesting they don't anticipate further downgrades in the near term.

Beyond the Headlines: The Technical Plumbing of Markets

For institutional investors and traders, the most critical questions revolve around how this downgrade will filter through market mechanics rather than headline sentiment. Several key transmission channels deserve attention:

Fixed Income Dynamics

Treasury bills and short-term repo markets should remain largely unaffected, as money market funds aren't generally rating-constrained for U.S. government securities. However, longer-dated Treasuries could see term premiums expand by 20 basis points as a baseline, with potential for 40 basis points if the tax cut legislation resurfaces.

Overview of the Repo Market

| Aspect | Details |

|---|---|

| Definition | Short-term collateralized loan involving sale and repurchase of securities |

| Key Participants | Banks, hedge funds, dealers, money market funds, central banks |

| Collateral Used | Typically U.S. Treasuries or other high-quality securities |

| Purpose | Provides short-term funding and liquidity |

| Importance | Supports liquidity, enables monetary policy, and stabilizes bond markets |

| Types of Repos | Overnight (1-day), Term (multi-day), Reverse repo (from lender's view) |

| Repo Rate | Implied interest rate based on buy/sell price difference |

| Central Bank Role | Uses repo/reverse repo to manage interest rates and inject/remove liquidity |

| Notable Event | 2019 U.S. repo rate spike led to Fed intervention via repo operations |

The municipal bond market faces more immediate challenges. AAA municipal scales have already begun slipping, with Maryland losing its Aaa rating earlier this week. Spread widening of 2-5 basis points has already materialized, with expectations that ratings migration will accelerate for agencies and large states tightly connected to federal funding flows.

Equity and Credit Implications

Duration-sensitive sectors like technology and utilities may feel pressure first if the yield curve continues steepening. Banks face a mixed outlook—higher net interest margins from a steeper curve but potentially larger unrealized losses on available-for-sale securities portfolios, which could reignite regulatory capital concerns.

Did you know? In finance, "duration" isn’t just a bond term—it also helps explain why certain equity sectors react more sharply to interest rate changes. Sectors like technology and utilities are considered “high duration” because their valuations rely heavily on future earnings, which lose value when interest rates rise due to higher discounting. In contrast, sectors like financials or energy are less sensitive—or even benefit—as rising rates can boost profit margins or have little impact on their near-term cash flows. So, interest rate shifts don’t just move bond prices—they ripple through the stock market in surprisingly sector-specific ways.

As one portfolio manager noted: "High-beta cyclicals like autos and industrials had already begun discounting a tariff-induced slowdown. The downgrade simply adds another catalyst for multiple compression in these sectors."

Dollar Dominance and Alternative Havens

Perhaps most telling is the evolving relationship between the U.S. dollar and traditional risk metrics. The correlation between the DXY dollar index and the VIX volatility index has turned negative for the first time since 2011—suggesting that during market stress, capital may increasingly flow to alternative havens like the Japanese yen, gold, and even cryptocurrency assets rather than automatically bidding up the dollar.

Did you know that while the U.S. Dollar Index (DXY) and the CBOE Volatility Index (VIX) have historically maintained a predominantly positive correlation-with the dollar typically strengthening during periods of market fear due to its "safe haven" status-this relationship took an unexpected negative turn in 2025? As of May 11, 2025, the DXY showed a year-over-year decline of -3.64% while the VIX simultaneously reached extreme levels not seen since 2020, closing at 52 on April 8, 2025, largely driven by the Trump administration's introduction of steep tariffs that created a geopolitical shock. This deviation from the historical pattern demonstrates how even established market relationships can temporarily break down during unique economic circumstances, though late April 2025 showed promising recovery signals as the VIX experienced a sharp decline from 50 to 30, which has historically indicated potential market recoveries if tariff threats remain contained and recession is avoided.

With foreign entities holding a record $9 trillion in Treasury securities, the system has tremendous inertia. However, marginal buyers—particularly sovereign wealth funds and emerging market reserve managers—may accelerate diversification plans into gold and Chinese yuan-denominated assets.

Strategic Implications for Key Stakeholders

The downgrade creates complex cascading effects across multiple financial constituencies:

For the U.S. Treasury, higher borrowing costs loom large. Every 25 basis point increase in rates adds approximately $90 billion to annual interest expenses by 2028, with net borrowing needs potentially exceeding $2 trillion annually. This could drive a heavier skew toward shorter-term bill issuance to manage costs.

The Federal Reserve may find its quantitative tightening program suddenly less benign if term premiums spike. Some analysts now predict balance sheet runoff could slow or halt entirely by 2026 if market functioning deteriorates.

For Congress and the White House, the political blame game intensifies, but the downgrade paradoxically improves the odds of a bipartisan fiscal reform package by 2026—though likely only after markets force the issue through more significant volatility.

Investment Playbook: Navigating the New Normal

For professional investors, several strategic positioning options emerge from this recalibrated fiscal landscape:

Near-term, fading the knee-jerk Treasury sell-off via futures looks attractive, particularly in the 3-5 year sector, as the "Fed put" remains intact for significant liquidity stress events.

Longer-term (12-24 months), underweighting 30-year Treasuries or implementing receive-fixed swap positions after a 20-30 basis point backup seems prudent as term premium repricing continues.

Alternative assets like gold and Bitcoin warrant increased allocation on price dips, supported by the emerging reserve-asset substitution narrative. Quality global investment-grade bonds from European and Swiss issuers may offer 15-20 basis point pickup versus U.S. counterparts when currency-hedged.

Within U.S. financials, a barbell approach favoring large-cap retail banking franchises while underweighting pure trading names could capitalize on steeper yield curves while minimizing mark-to-market risk on securities portfolios.

Did you know? The Barbell Investment Strategy blends opposites by allocating assets to both ultra-safe and high-risk investments—while skipping the middle ground. In bonds, it means holding short-term securities for safety and liquidity, alongside long-term bonds for higher yield, avoiding medium-term maturities. In equities, it might involve combining conservative assets like cash with aggressive plays like tech startups or options. This approach, popularized by Nassim Taleb, aims to protect against losses while still allowing for big upside—offering a strategic balance in uncertain markets.

The Long Game: From Credit Event to Structural Shift

While the immediate impact appears contained, the downgrade introduces what one macro strategist called "fat tails to every long-horizon valuation model." The path-dependent risks—including capital crowding-out, reserve currency erosion, and policy volatility—may fundamentally alter risk premiums over time.

Did you know? In finance, "fat tails" describe the higher likelihood of extreme market events—like crashes or surges—that traditional models often underestimate. Unlike the familiar bell curve, fat-tailed distributions suggest that rare, impactful events happen more often than expected. This has major implications: it means standard risk models can leave portfolios dangerously exposed, valuation tools may misprice assets, and financial systems need stronger safeguards. Events like the 2008 crisis or the COVID-19 crash are classic examples—reminders that in markets, the improbable is more probable than we think.

Some forward-looking scenarios gaining traction among institutional investors include the potential for a "Fed-Treasury Accord 2.0" if 10-year yields exceed 5.5% amid rising unemployment by 2027. This could introduce a soft form of yield curve management to cap long-term rates.

Did you know? The 1951 Fed-Treasury Accord marked a turning point in U.S. economic history by reasserting the Federal Reserve's independence from the Treasury. During World War II, the Fed had kept interest rates artificially low to help the government finance war debt, but postwar inflation forced a rethink. The Accord ended this policy, freeing the Fed to raise rates and fight inflation without being bound to the Treasury's borrowing needs. This agreement laid the foundation for modern central banking, where monetary policy is conducted independently to maintain price stability and economic health.

More radical innovations like blockchain-native Treasury bills by 2028 or smart-contract-style covenants in future issuance—possibly triggered by debt-to-GDP guard rails—represent low-probability but increasingly discussed options to restore market confidence.

"The downgrade is more a slow-burn credibility shock than an immediate funding crisis," concluded a sovereign debt specialist at a major asset manager. "Markets will adapt to an Aa1 America, but they'll increasingly price an option premium for political dysfunction—and that tiny wedge, compounded over years, has the potential to reshape global capital flows."

Did you know? "Bond vigilantes" are powerful investors who sell off government bonds when they believe fiscal policies are reckless—like excessive spending or soaring deficits—pushing bond prices down and yields up. This market pressure raises borrowing costs for governments and can force them to change course. The term, coined in the 1980s, reflects how these investors act like fiscal watchdogs, enforcing discipline through financial markets. From the U.S. bond rout in 1994 to the UK's mini-budget turmoil in 2022, bond vigilantes have shown they can influence national policy without casting a single vote.

For now, traders are positioning for modest near-term volatility while preserving capital for what many see as the real inflection point: when Washington next declares deficits "don't matter" but bond vigilantes finally disagree.